March 12, 2025

![]()

Europe’s self-storage market continues its upward trajectory, propelled by urbanization, housing shortages, and the evolving needs of businesses. As demand surges, the sector is emerging as a key player in the region’s real estate landscape. With over 13,000 facilities across the continent, self-storage is alleviating space constraints while attracting increasing investor interest. Despite this expansion, supply remains limited, creating significant opportunities for growth.

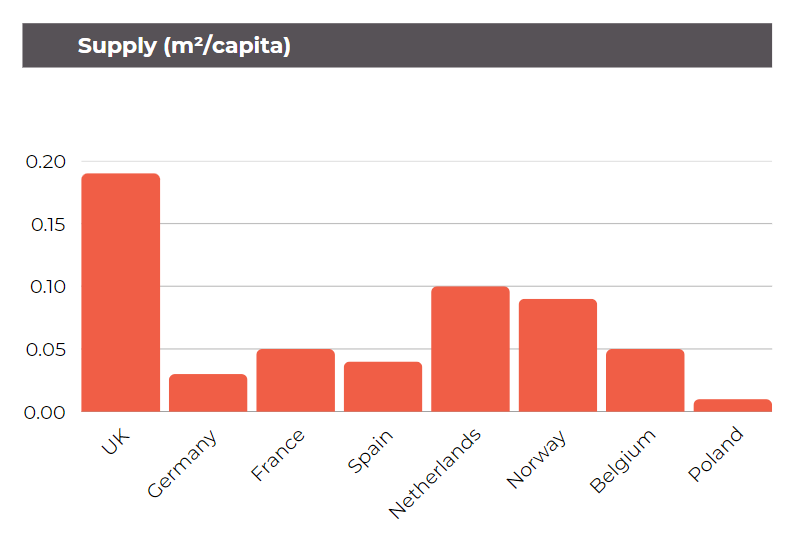

The UK leads the region with 0.19 square meters per capita, well ahead of mainland Europe. And as demand continues to rise combined with growing consumer awareness, the UK still holds substantial room for further expansion.

![]()

In mainland Europe, Germany, France, and Spain represent the three largest self-storage markets, collectively accounting for 52% of the region’s inventory. However, these markets remain severely undersupplied, making them key targets for institutional investment. Meanwhile, emerging markets like the Netherlands and Norway, are experiencing rapid growth, with supply per capita already exceeding that of the three largest markets, signaling a broader shift in investor focus toward high-growth opportunities.

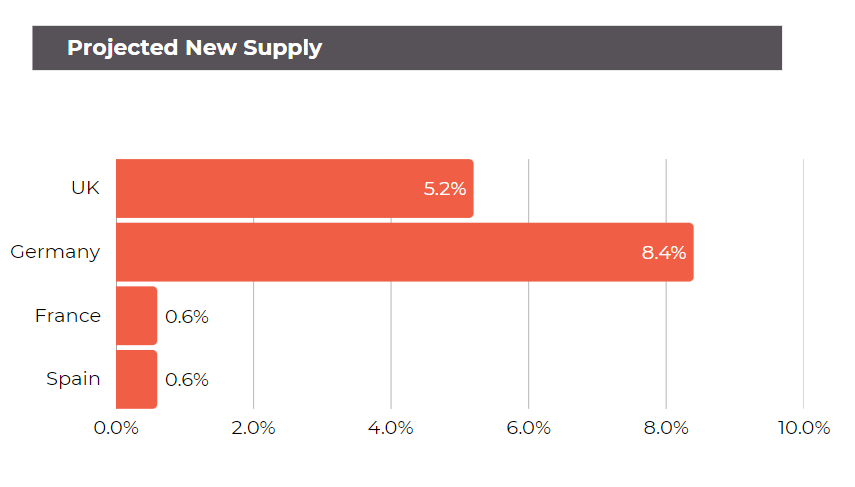

With demand outpacing supply, Europe’s self-storage market is poised for sustained expansion, driven by robust new supply growth in Germany (8.4%) and the UK (5.2%). Despite rising costs and economic uncertainties – including potential U.S. tariffs – the sector remains one of Europe’s most resilient and attractive alternative real estate assets. Bolstered by increasing institutional investments, strong consumer demand, and strategic acquisitions, the self-storage sector continues to showcase steady growth and long-term stability in an evolving economic environment.

*New supply data is based on published squared footage for projects under development and StorTrack’s estimates for projects where square footage information is unavailable.

![]()

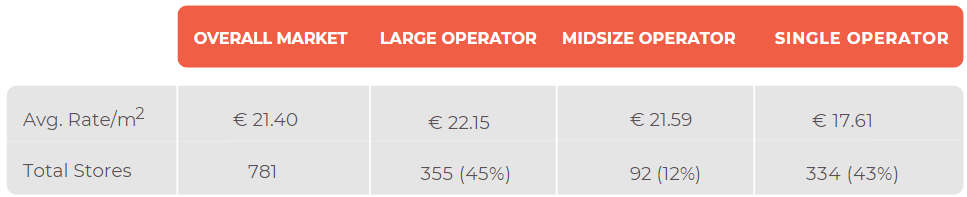

UNITED KINGDOM

UK self-storage continues its expansion, with prices up 3.4% YoY, fueled by high housing costs, compact living spaces, and the surge in e-commerce. While single operators still dominate over 60% of the market, larger players are gaining momentum, drawn by strong investment potential. For example, the planned sale of Access Self Storage (60 locations) has drawn bids from Aermont Capital, TPG Inc., and Shurgard, underscoring the increasing appeal of the sector to institutional investors. At the same time, operators are scaling rapidly to meet demand – Storage Giant Ltd. is adding 11 new locations across North Wales and North West England, while Cuboid is expanding its traditional self-storage offering into new container types. As institutional capital accelerates and established operators expand their footprint, the UK remains one of Europe’s most dynamic and investible self-storage markets.

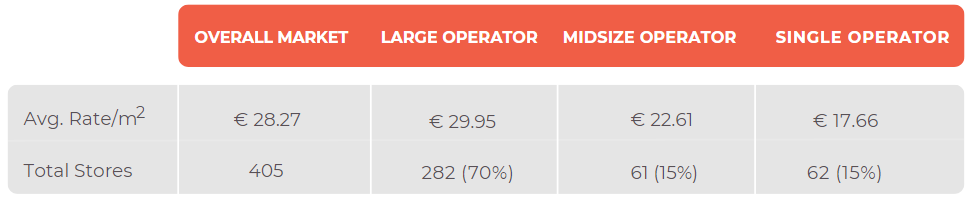

GERMANY

Germany’s self-storage market is also expanding, fueled by urbanization, rising incomes, small business expansion, and increasing public awareness. Supply is growing as companies like Sirius Real Estate, a leading owner/operator of business parks in the UK and Germany, integrates self-storage into its growth strategies, developing new facilities in Berlin and repurposing existing sites to meet demand. Even with increasing competition, rates have risen over 10% in the past year, highlighting strong market fundamentals.

FRANCE

France’s self-storage market continues to grow, with key urban centers like Paris, Lyon, and Marseille experiencing rate increases from 1.4% in Marseille to over 9% in Paris, even as new supply enters the market. With over 20,000 square meters of development in the pipeline, additional inventory could begin to impact pricing. At the same time, institutional investment is accelerating as larger players like PGIM Real Estate and Pithos Capital expand their footprint, securing six assets and building a strong acquisition pipeline. As investor interest grows and market potential evolves, self-storage in France becomes an increasingly prominent part of the real estate sector.

SPAIN

Price trends in Spain have been mixed, with urban demand in Madrid and Barcelona driving YoY growth exceeding 5%, while seasonal tourism fluctuation and rising supply have led to localized pricing shifts in some areas. The ongoing trends of urbanization, smaller living spaces, and housing affordability challenges continue to drive the need for flexible storage solutions.

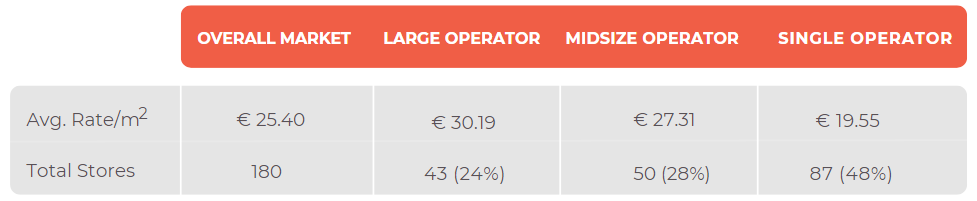

NETHERLANDS

Despite new supply entering the market, rates increased by an average 1%, reflecting steady demand. As one of Europe’s fastest growing self-storage markets, the Netherlands has seen 11 new facilities open in the past year, and is expected to receive over 20,000 square meters of new development over the next 12 months. The market is currently divided between large operators and single-location owners, each holding just over 40% of total supply. However, this balance is shifting as larger players expand their presence, especially in urban areas. Like other major European markets, urbanization, e-commerce growth, and space constraints continue to drive demand.

NORWAY

Norway self-storage market is rapidly evolving, driven by high urbanization, rising housing costs, and a robust economy that supports strong purchasing power. With large operators controlling 70% of the market, facilities are heavily concentrated in major cities like Oslo and Fredrikstad, where space constraints and steady consumer demand continue to drive market growth.

BELGIUM

Belgium’s self-storage market remains stable, with prices holding steady over the past year. While nearly half the market is made up of smaller independent operators, limited new supply has sustained price stability. However, if development accelerates, competitive pressures could impact pricing dynamics.

POLAND

Poland remains one of Europe’s most underpenetrated self-storage markets, attracting heightened investor interest as major operators expand their footprint. With supply per capita still remarkably low, the market’s untapped potential presents a compelling opportunity for long-term growth and strategic expansion. Growing urbanization, the rise of e-commerce, and increasing consumer awareness drive demand, prompting at least 11 new development projects that will add over 19,000 square meters to current supply.

While price movements vary across markets, supply growth, urbanization trends, and macroeconomic factors continue to influence pricing dynamics. Despite headwinds from inflation and interest rate uncertainty, demand fundamentals remain strong in core and emerging markets alike.

![]()

Investor confidence in European self-storage remains strong, with major acquisitions and expansion efforts accelerating across both mature and high-growth markets. Amid macroeconomic uncertainties, institutional investors continue targeting underpenetrated regions, drawn by the sector’s resilience and enduring demand fundamentals.

Western and Southern Europe are seeing a surge in investment, exemplified by Safestore ‘s expansion into Italy through a joint venture with Nuveen Real Estate, acquiring Easybox, the country’s second-largest operator. In Sweden, Heitman’s majority stake acquisition in Servistore highlights the market’s significant growth potential amid limited supply (0.07 SQM per capita). Meanwhile, Poland, Belgium, and the Netherlands continue to attract new developments and institutional capital, cementing their status as key growth markets.

While rising construction costs and regulatory hurdles in cities like London and Paris pose challenges, investors are adapting by expanding into underserved markets, developing specialty storage solutions, and improving operational efficiencies. Market consolidation, automation, and strategic asset development will shape the next phase of European self-storage growth, ensuring its position as a resilient and competitive real estate sector.

As investment deepens and demand remains strong, Europe’s self-storage landscape is evolving from a fragmented market into a more sophisticated, institutionalized asset class, poised for sustained long-term growth.

![]()

StorTrack is the leading provider of self-storage market data and insights, enabling operators, investors, and developers to make informed, data-driven decisions. Since 2014, StorTrack has delivered accurate, actionable market analytics to self-storage professionals worldwide.

With coverage spanning over 4,700 facilities in the UK and more than 8,000 across 23 European countries, StorTrack offers access to market trends, rate data, and development insights. StorTrack’s tools, including the Explorer platform, custom reports, and API, provide clarity on market feasibility, competitor pricing, and demand trends, helping self-storage professionals stay ahead in a rapidly evolving industry.

Whether you’re optimising pricing strategies, assessing market opportunities, or expanding your portfolio, StorTrack is your trusted partner for success in the self-storage sector in Europe and beyond.

![]()